VSME Supporting guide on Disclosure C3 – Comprehensive Module (GHG reduction targets and climate transition)

THE CONTENT OF THIS SUPPORTING GUIDE IS PREPARED FOR UNDERTAKINGS WITH FEWER THAN 250 EMPLOYEES, IT IS NOT MANDATORY AND SERVES TO GUIDE THOSE UNDERTAKINGS THAT HAVE DECIDED TO DISCLOSE GHG EMISSIONS REDUCTION TARGETS AND CLIMATE TRANSITION PLANS

Disclaimer

The European Commission in the Omnibus proposal released on 26 February 2025 proposes, to use the VSME Standard as the basis of a future voluntary standard for undertakings up to 1000 employees. The VSME Standard has been developed for use by undertakings with fewer than 250 employees including micro-enterprises and has not been tested for use by other larger and more complex undertakings. It is important to note that on 30 July 2025 the European Commission officially adopted EFRAG's VSME as a Recommendation for use by undertakings with fewer than 250 employees.

No information is available at the moment with regard to the issuance of a proportionate voluntary standard to be adopted by the Commission as a delegated act, based on the VSME standard, to be used for undertakings with more than 250 employees but excluded from the scope of the CSRD.

The VSME supporting guides currently being developed are to be understood as supporting the application of the VSME Standard for undertakings with fewer than 250 employees. The content of this VSME supporting guide has been developed in line with the scope of the VSME. Consistency checks and adjustments may be needed in light of development under omnibus and revised ESRS

Introduction and aim of the Supporting Guide

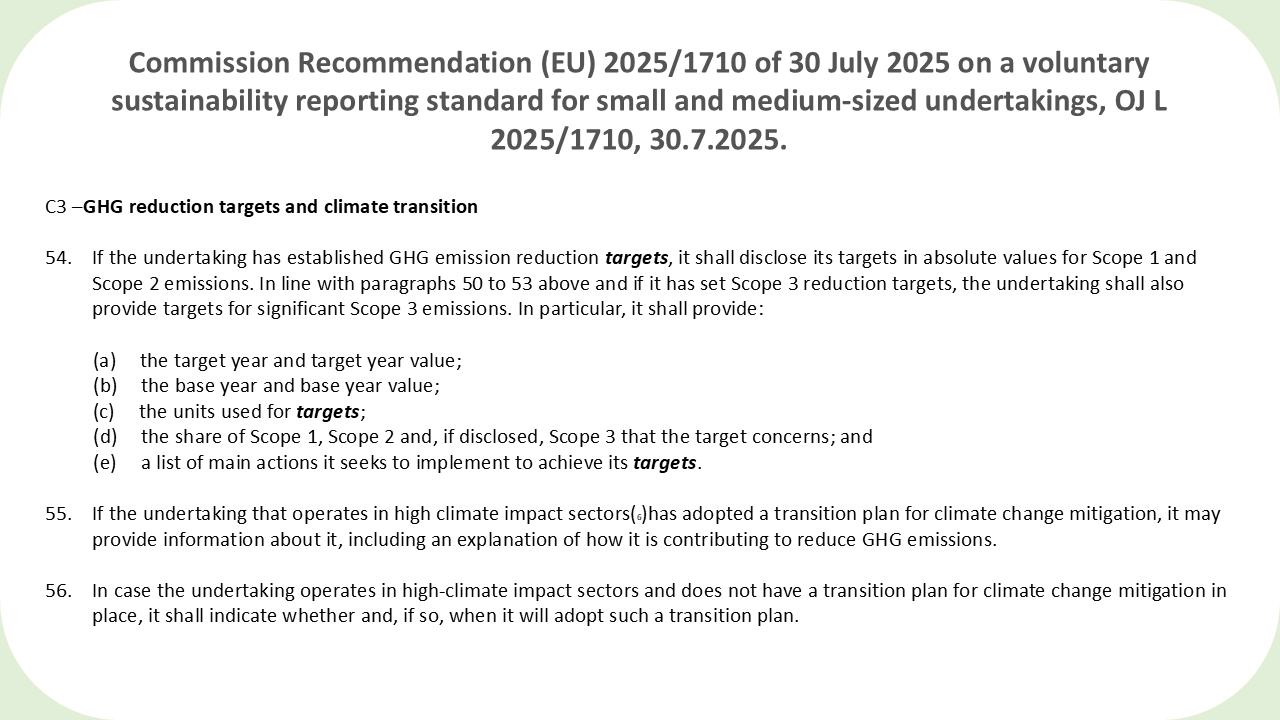

This supporting guide is only intended for undertakings that have decided to adopt and disclose GHG emissions reduction targets and /or climate transition plans. This Supporting Guide provides step-by-step guidance on how to structure and report GHG reduction targets and climate transition plans according with disclosure C3 of the VSME Standard (see extract below).

This Supporting Guide is divided into two sections:

Provides guidance for small and medium undertakings setting GHG emissions reduction targets, including relevant actions/practices to achieve them.

Provides guidance for small and medium undertakings operating in high-climate impact sectors that have decided to adopt a climate transition plan (see section 2 for high-climate impact sector classification). Section 2 builds upon and complements Section 1, so it should be read conjunctively with Section 1.

Scope 3 GHG emissions fall outside the scope of this guide. However, undertakings that choose to include Scope 3 should apply the same logic used for Scope 1 and Scope 2 when setting GHG emission reduction targets, and, where relevant, integrate these targets into their transition plans.

This guide is intended as a work in progress with possible updates in the near future, particularly with regard to a guide on Scope 3 emissions, which may be of interest to undertakings operating in manufacturing, agri-food, real estate construction and packaging processes, where Scope 3 is likely to be significant. This would serve to overcome the difficulties and costs that those undertaking may face in reporting Scope 3 emissions-related targets. This work is also connectedwith EFRAG’s ongoing mapping of digital GHG calculators and depends on the maturity in the market as undertakings gain knowledge and preparedness on this metric.

Introduction to GHG reduction targets and transition plans

Adopting GHG emission reduction targets is an important step in the transition to a sustainable economy, as it enables undertakings to manage change in a systematic, controlled, and organised manner.

For undertakings active in high-climate impact sectors, where decarbonisation investments are likely to be higher, or certain activities are difficult to decarbonise, achieving targets may benefit from implementing a comprehensive transition planning process that supports change management and internal decision-making.

Section 1:

GHG reduction targets

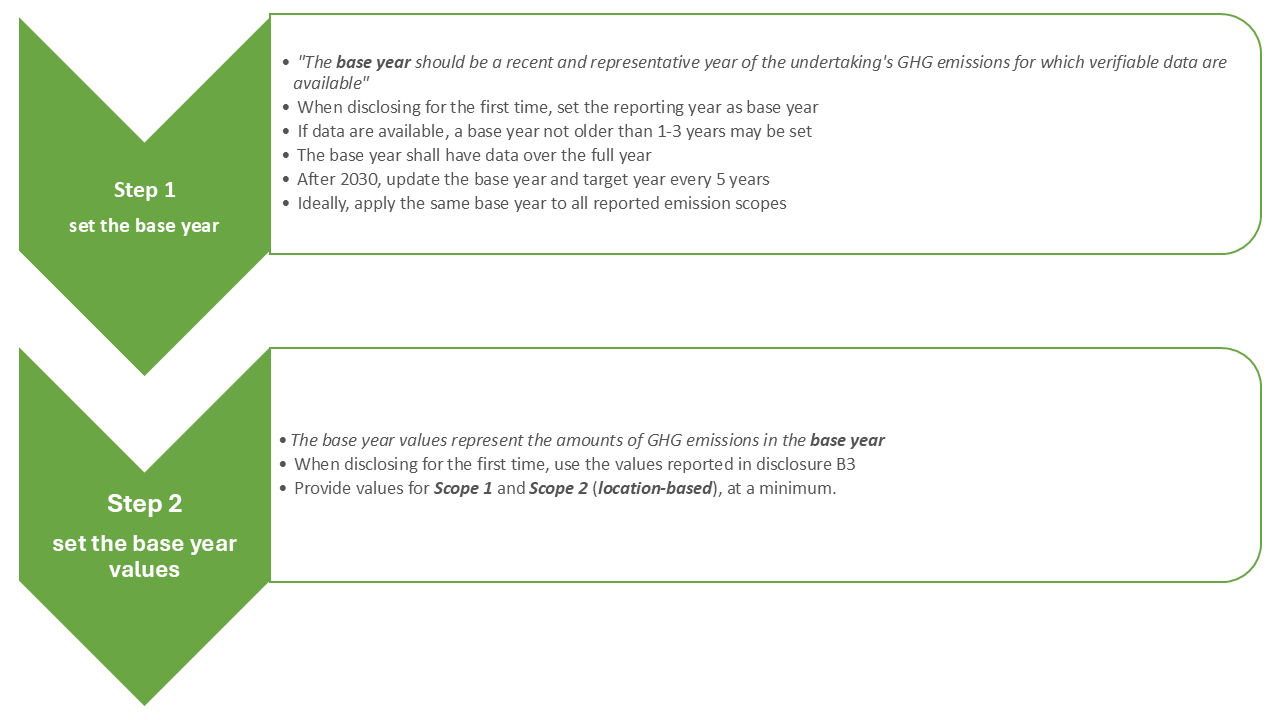

"A GHG reduction target is a commitment to reduce the GHG emissions in a future year compared to the emissions measured during a chosen base year" |

The standard does not require companies to set targets. However, it is considered good practice for companies to set Scope 1, Scope2, (and Scope 3) targets for 2030. If companies do set targets, the standard requires them to be disclosed. Guidance on CO2 emission sources and the definition of Scope 1, Scope 2, (and Scope 3) can be found in the guidance of the VSME Standard (Annex II paragraph 26-45).

All amounts of GHG emissions should be expressed in tons of CO2 equivalent (tCO2eq) as required by disclosure B3 (§30, Annex 1). Undertakings shall disclose their estimated GHG emissions in disclosure B3 when reporting targets.

GHG removals (e.g. removing CO2 from the atmosphere through afforestation), avoided emissions (e.g. GHG emissions avoided through the sale of insulation products) and offsetting through carbon credits (e.g. compensation programs outside the undertaking’s value chain) shall not be counted when calculating GHG emissions or setting the undertaking’s gross GHG emission reduction targets, as specified in paragraph 154-155 (Annex 2) of the VSME Standard.

Step-by-step guide to disclosing GHG reduction targets

This section provides a step-by-step guidance on setting GHG emissions reduction targets, with particular attention to undertakings setting targets for the first time. The supporting guide aligns with the VSME’s disclosures.

- Setting the timeframes

- Setting the ambition level

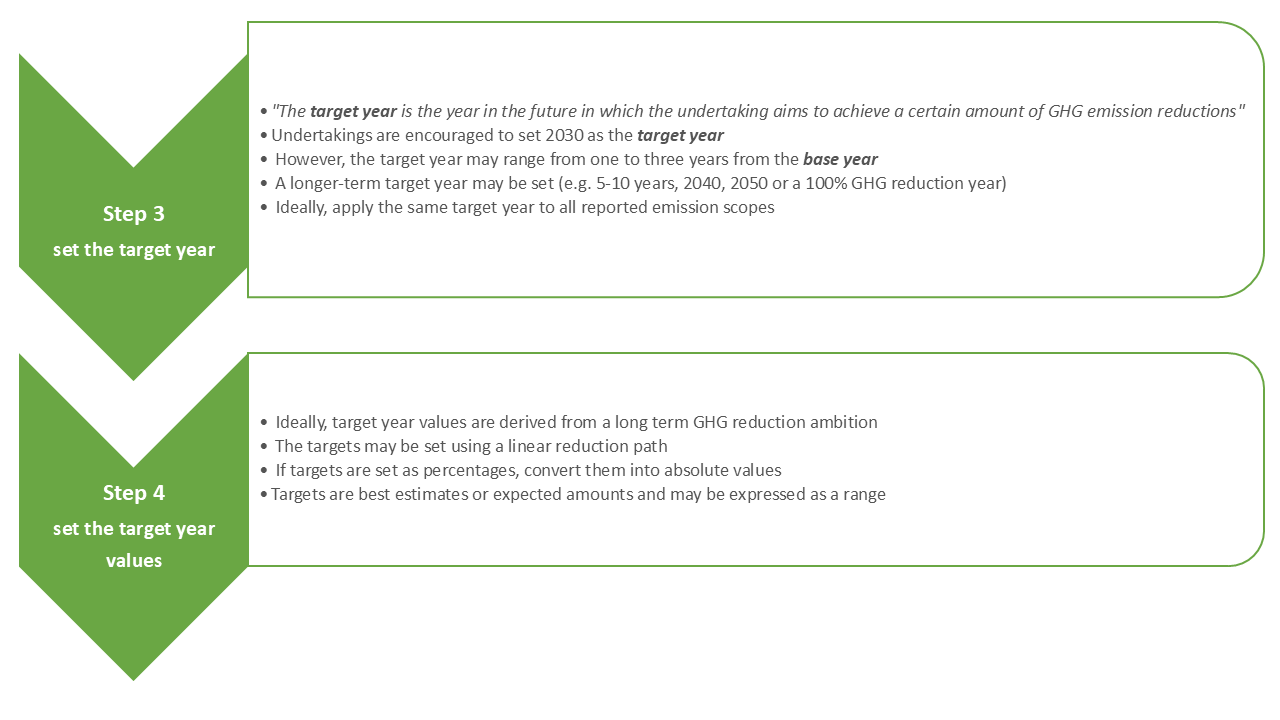

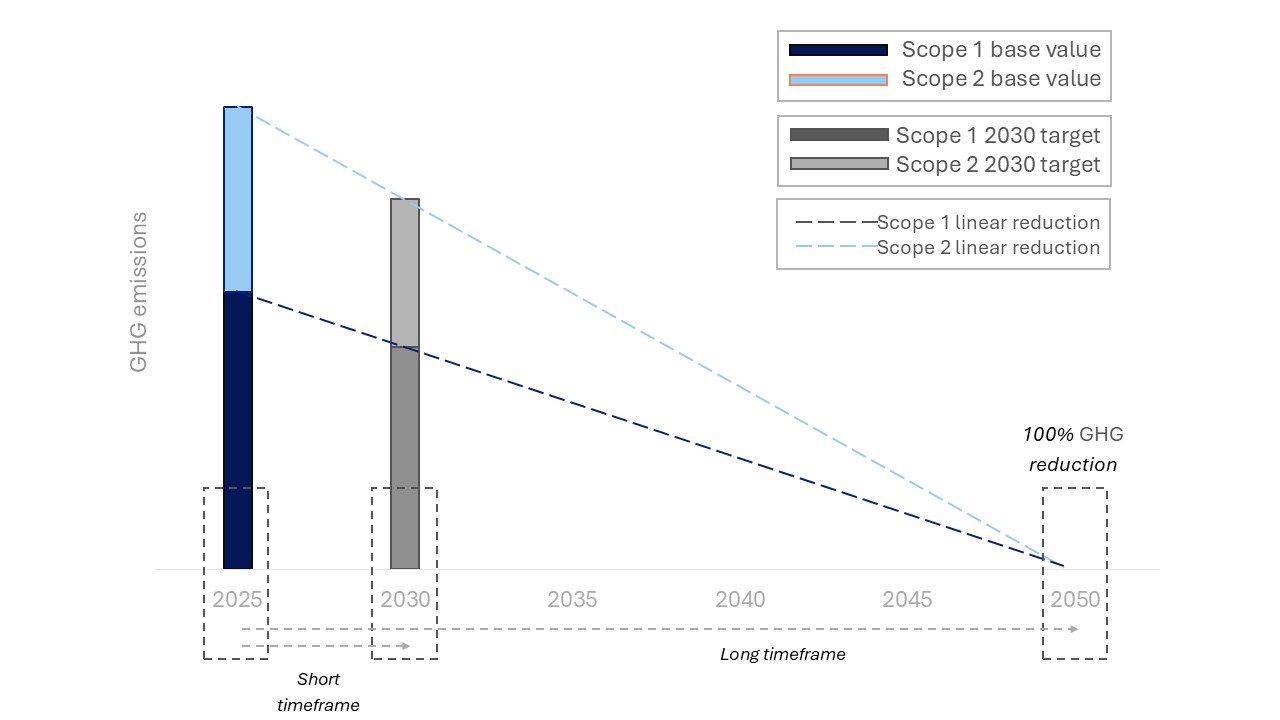

The graphic below illustrates how undertakings can set a target using a linear emission reduction path. In this approach, the undertaking defines the desired emission level (“target value”) and the year by which it aims to achieve it (“target year”). The example shows a long-term ambition of 100% GHG emissions reduction by 2050 to help establish the linear reduction pathway. From this pathway, Scope 1 and Scope 2 emissions can be directly derived.

Scope 2 emissions can be reported using two methods: location-based and market-based. While the VSME Standard requires the disclosure of Scope 2 emissions using the location-based method, it is useful for companies to disclose both. When using the location-based method, Scope 2 emissions can mainly be reduced through energy efficiency measures or by consuming self-generated renewable energy. In addition to the two primary levers for reducing Scope 2 emissions, energy efficiency and on-site renewable generation, undertakings can also report using the market-based method. This allows them to purchase renewable electricity and apply a lower market-based emission factor, thereby reducing their reported Scope 2 market-based emissions. Purchasing renewable electricity is a relatively low-effort way to decrease market-based Scope 2 emissions and contributes to climate change mitigation.

It is important to stress that fast-growing undertakings (especially those in high-climate impact sectors) are expected to disclose absolute GHG emission reduction targets while acknowledging that their organic growth may lead to higher uncertainties about future emission levels.

This simplified approach does not account for the fact that different business activities are likely to decarbonise at different rates through 2050. A non-linear approach may provide a more accurate representation of decarbonisation efforts and targets. For example, in service undertakings, electricity use can often be decarbonised more easily by acquiring a renewable Power Purchase Agreement (PPA) or purchasing Guarantees of Origin (GOs) which could justify a more ambitious Scope 2 emissions target.

Target setting example

An SME disclosing for the first time sets the base year as the (current) reporting year (2025), and chooses 2030 as the target year.

It also decides to reduce Scope 1 emissions by electrifying part of its fleet, targeting a reduction of approximately 35% of Scope 1 emissions. This will shift some GHG emissions to Scope 2, as more electricity will required to power the electric vehicles (+33% in Scope 2 location-based emissions).

The undertaking decides to procure only renewable electricity by 2030, fully decarbonising its Scope 2 market-based emissions. The purchase of renewable electricity does not impact location-based Scope 2 emissions as these reflect the grid’s electricity mix.

The total GHG reduction target indicates that the undertaking aims to reduce Scope 1 and Scope 2 (market-based) emissions with 110t CO2eq by 2030, corresponding to a 48% reduction from the base year. The undertaking can calculate these reductions using simple assumptions based on current electricity bills, fuel purchase records, or vehicle mileage. These provide a practical basis for estimating progress over time and tracking future emissions.

Example of target setting for an SME

| Target setting example | Baseline | Current report | Target (2030 encouraged) | % change |

Year | 2025 | 2025 | 2030 | |

Scope 1 (tCO2eq) | 185 | 185 | 120 | -35% |

Scope 2 location-based (tCO2eq) | 45 | 45 | 60 | +33% |

Scope 2 market-based (tCO2eq) | 45 | 45 | 0 | -100% |

Total (tCO2eq) Scope 1&2 location-based | 230 | 230 | 180 | -22% |

Total (tCO2eq) Scope 1&2 market-based | 230 | 230 | 120 | -48% |

Main actions to implement the targets

While disclosing information on the main GHG reduction actions to achieve the targets, undertakings may refer to disclosure C2 to align with the practices, policies, or future initiatives contributing to climate change mitigation. A specific supporting guide on disclosure C2 provides an non-exhaustive list of illustrative examples for climate mitigation actions that may be considered as implementing actions for GHG reduction targets.

It is expected that these actions are subsequently categorised as contributing to Scope 1 and Scope 2 reduction targets, ideally differentiating between location-based and market-based emissions reductions, as shown in the example illustrated in Box 1 below.

Scope 1: Low-carbon transport Our actions include retiring depreciated diesel vans and replacing them with new electric vans (e-vans). In addition, cargo bikes will be leased in alignment with the SME’s growth strategy to further reduce greenhouse gas emissions. Scope 2: Energy efficiency measures We plan to upgrade machines to A-label energy-efficient models according to their depreciation schedule, ensuring a gradual transition to lower energy consumption. Scope 2: Renewable energy – renewable electricity sourcing To reduce reliance on fossil fuels, 50% of the SME’s electricity will be sourced from renewable electricity providers via a Power Purchase Agreement (PPA), thereby reducing Scope 2 market-based emissions. |

Box 1: Example of main action to implement the undertaking's GHG reduction targets

Section 2:

Step-by-step guide to a climate transition plan

| IMPORTANT: This section applies specifically to undertakings operating in high-climate impact sectors. Other companies such as those operating in the services sector are not expected to draft or disclose transition plans. Those wishing to do so also may follow the guidelines below (e.g. data centres). |

Table 1 provides an overview of the high-climate impact sectors as defined by the VSME standard.

Table 1 High climate impact sectors (VSME standard, §55, NACE v2.1 classification)

Class | Description |

A | Agriculture, Forestry, and Fishing |

B | Mining and Quarrying |

C | Manufacturing |

D | Electricity, Gas, Steam, and Air Conditioning Supply |

E | Water Supply, Sewerage, Waste Management, and Remediation Activities |

F | Construction |

G | Wholesale and Retail Trade, Repair of Motor Vehicles and Motorcycles |

H | Transportation and Storage |

M | Real Estate Activities |

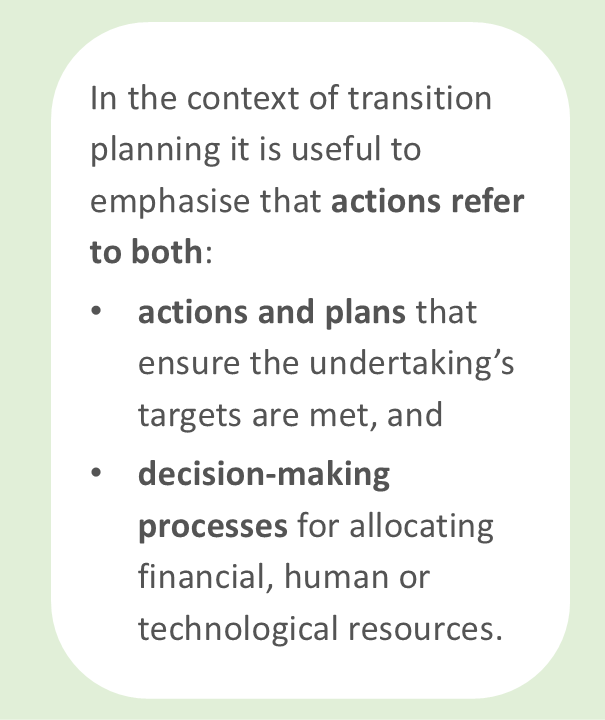

A transition plan for climate mitigation is the part of an undertaking's strategy that defines its GHG reduction targets, supported by a set of current and future actions, ensuring alignment with the transition to a lower-carbon economy and with the EU climate commitments to limit global warming.

Transition planning is an ongoing effort, not a one-time effort. The plan can be expected to evolve as market conditions, policies, and risks change, and it should be reviewed periodically. A credible transition plan for climate mitigation includes a list of actions to be implemented over a time horizon, taking the undertaking's financial planning into account.

This transition plan will have to be updated on a regular basis as not all planned actions may be implemented, in particular those actions that depend on uncertain future developments (e.g. price changes, liquidity).

Undertakings are not expected to disclose their full transition plan. A summarised version is sufficient, provided it allows users of the VSME report to assess GHG reductions, timeline and its financial implications.

The combination of the elements illustrated below ensures that a transition plan is disclosed in a credible manner:

Case study – setting the scene

To clarify the disclosure expectations, a case study of SME A, which operates in a high-climate impact sector, is provided throughout the transition plan guidance.

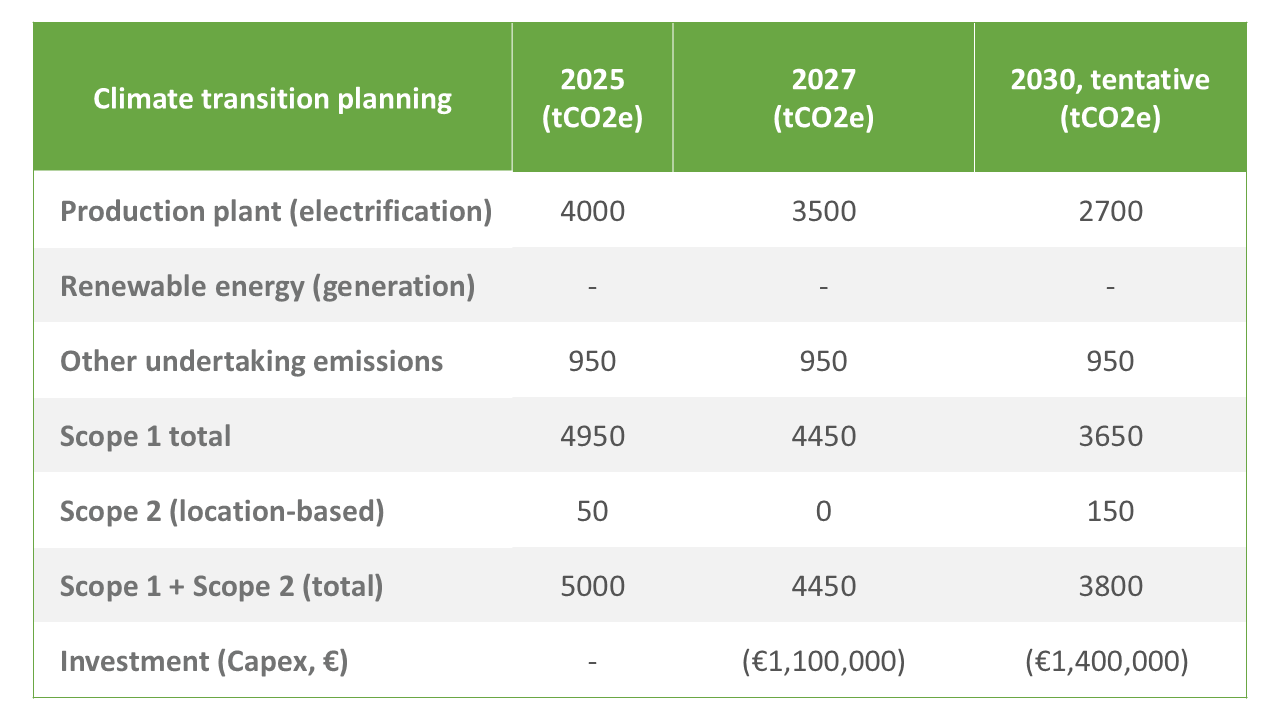

SME A is active in a climate-intensive sector and has set emission reduction targets aimed at lowering total GHG emissions from 5000 tCO2eq in 2025 (disclosure B3) to 3850 tCO2eq by 2030 (disclosure C3 GHG reduction targets), representing a 23% reduction. The SME has also identified a list of GHG-reduction actions, as required in disclosure C3, and has detailed the main actions planned to implement these targets.

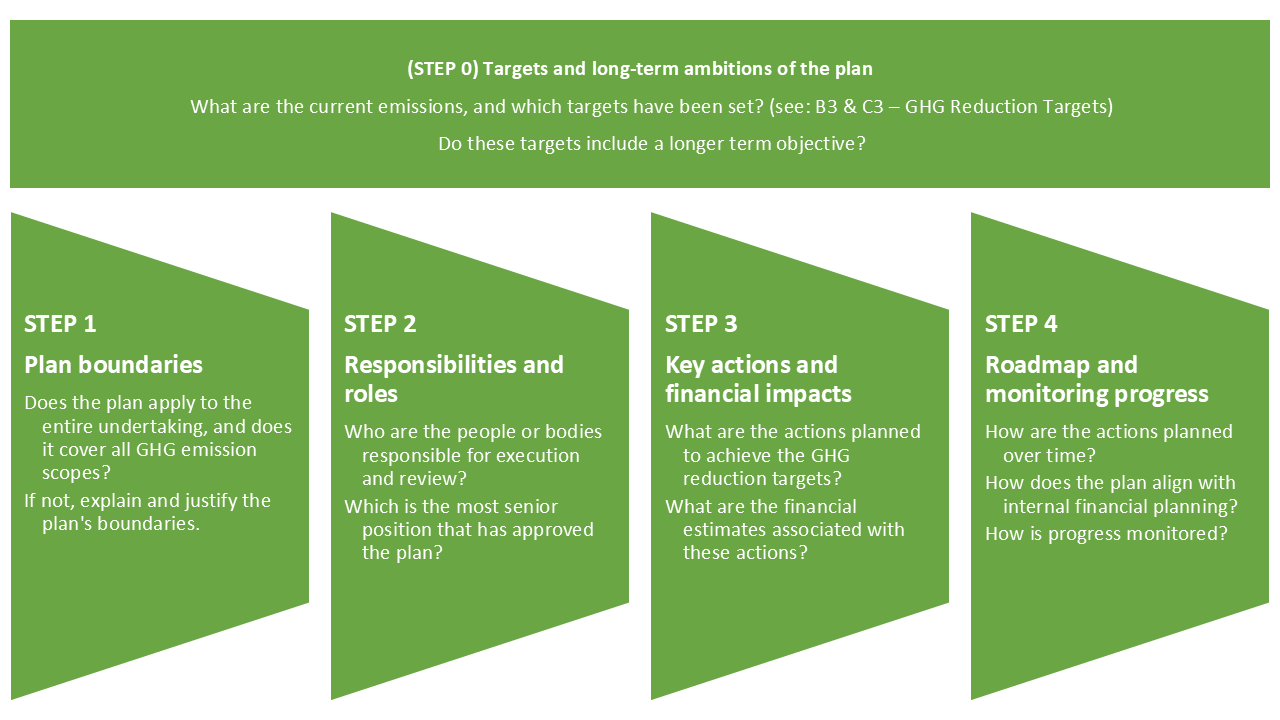

Step 1. Scope of the plan

A transition plan for climate change mitigation developed by an undertaking may cover all of its emissions (disclosure B3) and targets (disclosure C3), or only a portion of them. After measuring its emissions, an undertaking can decide for strategic reasons to limit the extent of the plan to, for example, specific high-emitting activities or to a specific time horizon, as illustrated in the case study below.

Case study – boundaries of the transition plan

SME A discloses that its current GHG emission reduction target for 2030 would imply a further future GHG emissions reduction of more than 90% by 2050 if it were to continue decarbonising at the same rate. However, it clarifies that it has not yet set a longer term target, as it first needs to gain more experience in reducing GHG emissions. The SME also discloses that the plan focuses primarily on the electrification of its production process, since the current production process accounts for the majority of its known GHG emissions (80%), mainly due to its gas-fired dryers and furnaces and because this represents the largest financial challenge. SME A further states that Scope 3 emissions are currently not disclosed in the plan, as no reduction targets have yet been set for Scope 3.

It is expected that the transition plan clearly lays out the boundaries of the transition plan, explaining what is included, in terms of undertaking sites, activities or installations, as well as the timeframe, and whether all emission scopes are considered. The undertaking is also expected to provide an explanation of why these boundaries were considered.

Step 2. Responsibilities and roles

For a successful transition plan for climate mitigation, leadership commitment is crucial. Responsibility for the plan usually lies with the most senior level of the undertaking accountable for its implementation. Depending on the size and complexity of the undertaking, the governance and execution of the plan can lie with one, multiple people, or even with working groups. This means that the owners, key decision-makers like a management board, or specific climate governance groups can set the ambition level of the plan. The implementation of specific actions can be assigned to the same roles, or to specific experts such as the environmental manager, or project leads.

Case study – governance of the plan: who does what?

SME A discloses that the plan has been approved by undertaking’s management. The managing director is responsible for setting and monitoring the SME’s climate transition priorities, while the operations manager ensures effective implementation. The SME has asked its accounting service provider to support the annual financial risk assessment of the plan and to assist with future reviews of the plan’s priorities.

Step 3. Disclose key actions and financial impacts

In this step, undertakings should discuss the GHG reduction potential and the financial impacts of the key actions they identified for reducing GHG emissions.

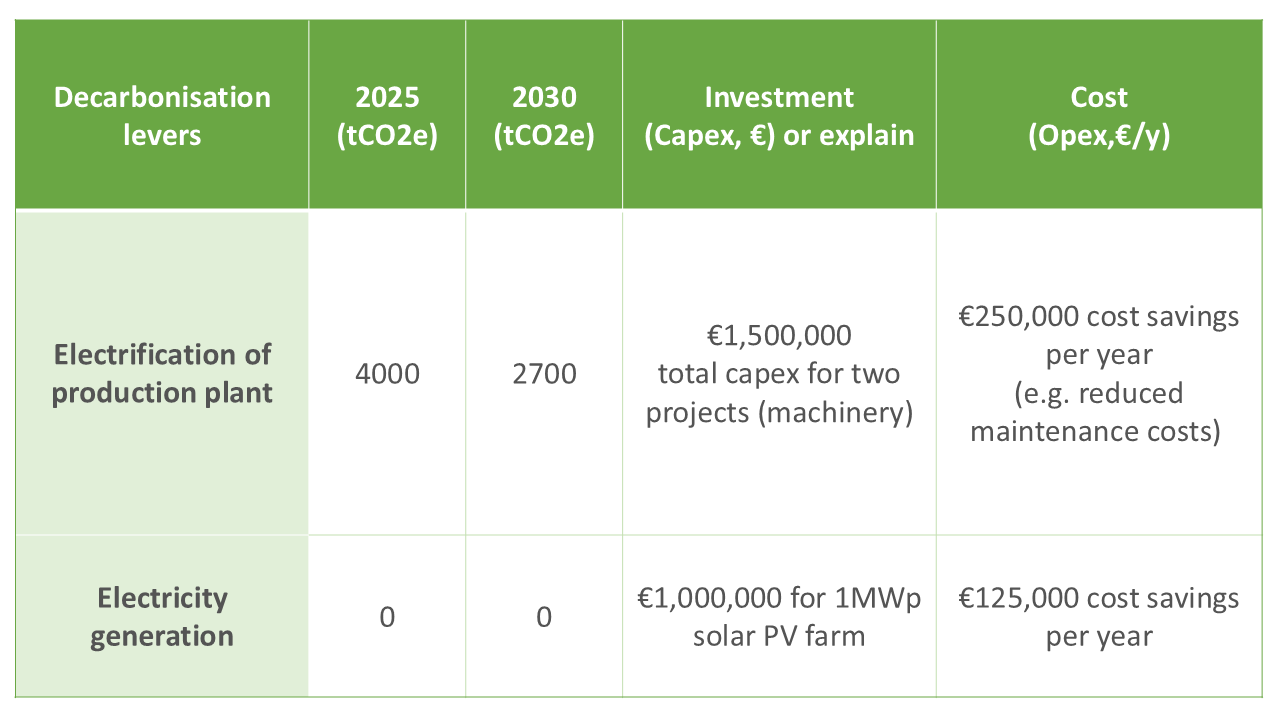

If an undertaking has identified a long list of actions, it may aggregate these actions into decarbonisation levers. Examples of such levers can be found in the climate change mitigation categories outlined in the Supporting Guide on disclosure C2.

Decarbonisation levers are higher-level, aggregated types of actions such as “energy efficiency”, “electrification”, “use of renewable energy”, “redesign of products” that group individual climate change mitigation actions and that help the undertaking communicate key strategic decarbonisation options.

A credible transition plan has to consider the financial planning cycle of the undertaking. For planned actions expected to occur beyond the current financial planning horizon, the undertaking may provide approximations of GHG reductions and the financial resources required for future implementation.

Note that GHG removals (e.g. carbon credits from compensation programs like reforestation) and avoided emissions (e.g. GHG emissions avoided because of selling insulation products) cannot be included in the list of actions to reduce GHG emissions and achieve targets. For further elaboration please consult §154-155 (Annex 2) of the VSME Standard.

CONSIDERATIONS ON CAPEX/OPEX AND OTHER FINANCIAL INDICATORS

CapEx represents upfront investments, such as purchasing energy-efficient equipment or installing renewable energy infrastructure, which may require significant funding but can deliver to long-term cost savings and improved efficiency. OpEx, on the other hand, includes operating costs such as maintenance, energy procurement, and operational adjustments, which must be managed to ensure the financially viable implementation of their climate initiatives.

Other financial indicators can also provide useful information. The payback period, for example, shows how long it takes to recover the initial investment. A more advanced measure is the internal rate of return (IRR), which expresses the annual return on an investment. Both indicators can help evaluate how attractive the investment is and guide decisions on which projects to prioritise.

Step 4. Disclosing the roadmap and monitoring progress

SMEs may present their GHG emission reduction targets and decarbonisation levers either in a table or graphically, illustrating developments over time.

Case study – disclosing the transition plan and monitoring progress

SME A has a financial planning cycle of 2 years. It decides to set interim targets for 2027 in line with the undertaking’s financial approach. As a first step, a relatively modest electrification project is selected to demonstrate the economic viability of the transition. Additionally, the development of half of the planned solar PV installation is scheduled for 2027 due to the complementarity with the existing energy portfolio. Approximately € 1.1 million in investments are planned to achieve these interim targets by 2027, with further planned investments of another € 1.4 million in 2030.

SME A also provides a tentative outlook to 2030 to start discussions with prospective investors.

Progress of the plan can be monitored through the performance of the solar PV installation which is expected to supply sufficient energy for the operation of the first electric furnace between 2027 and 2030. The managing director will evaluate the annual progress of the plan. Additionally, considering the undertaking’s current growth trajectory, the managing director will evaluate on an annual basis whether additional actions are required to remain on track to achieve the target commitments.