VSME Supporting Guide on Disclosure C2- Comprehensive Module (Practices, Policies, and Future Initiatives)

THE CONTENT OF THIS SUPPORTING GUIDE IS PREPARED FOR UNDERTAKINGS WITH FEWER THAN 250 EMPLOYEES

Disclaimer

The European Commission in the Omnibus proposal released on 26 February 2025 proposes, to use the VSME Standard as the basis of a future voluntary standard for undertakings up to 1000 employees. The VSME Standard has been developed for use by undertakings with fewer than 250 employees including micro-enterprises and has not been tested for use by other larger and more complex undertakings . It is important to note that on 30 July 2025 the European Commission officially adopted EFRAG's VSME as a Recommendation for use by undertakings with fewer than 250 employees.

With regard to the issuance of a proportionate voluntary standard to be adopted by the Commission as a delegated act, based on the VSME standard, to be used for undertakings with more than 250 employees but excluded from the scope of the CSRD. The VSME supporting guides currently being developed are to be understood as supporting the application of the VSME Standard for undertakings with fewer than 250 employees. The content of these VSME supporting guides has been developed in line with the scope of the VSME. Consistency checks and adjustments may be needed in light of development under omnibus and revised ESRS.

Introduction

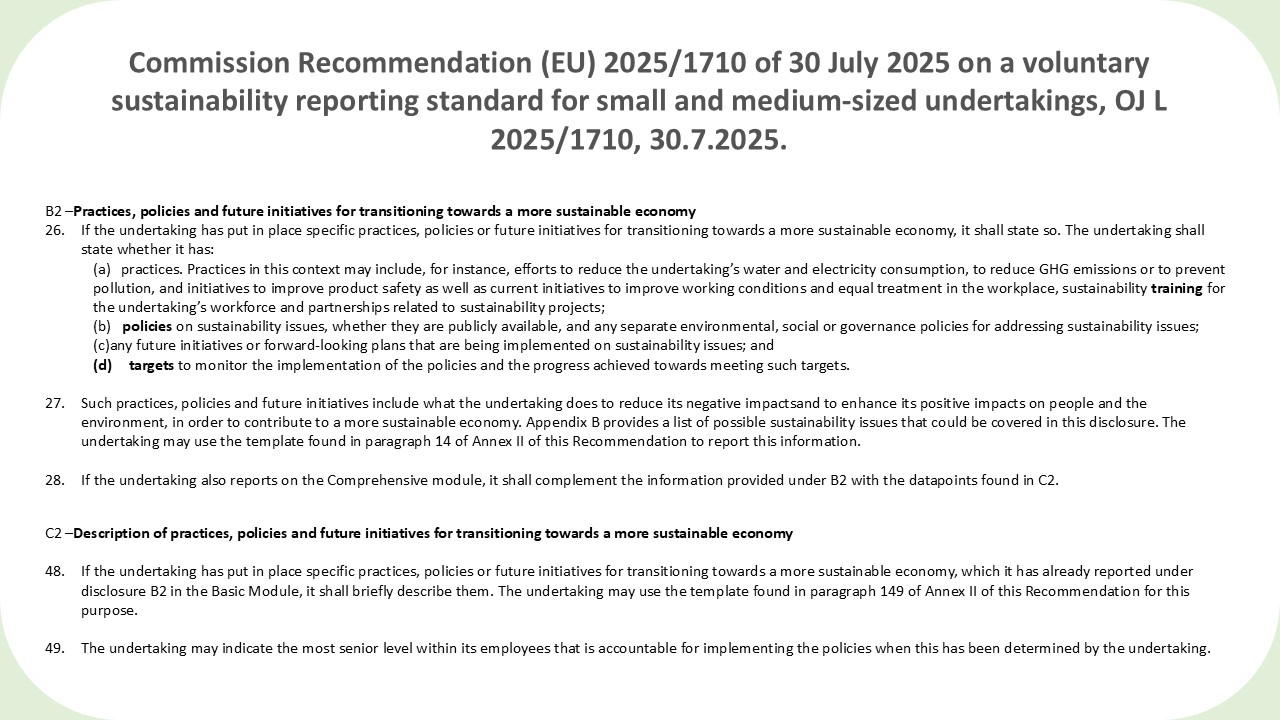

This supporting guide complements disclosure C2 - Description of practices, policies and future initiatives for transitioning towards a more sustainable economy (paragraph 48, 49) of the VSME.

Disclosure C2 builds upon disclosure B2 (Basic Module). In disclosure B2, the undertaking is asked to disclose whether it has practices, policies and future initiatives that tackle the list of sustainability issues (Annex B of the VSME). In disclosure C2, undertakings are asked to describe this information. An extract of both disclosures is displayed on the right.

Structure and aim of the supporting guide

| The content of this supporting guide is non-mandatory, non-exhaustive, non-binding, or prescriptive. This supporting guide does not set any expectations for the specific content to be reported, but aims to help SMEs by providing possible elements for their disclosures. |

This supporting guide is composed of two sections:

- Section 1: List of examples of practices, policies and future initiatives by sustainability topics

- Section 2: Case studies

Practices (paragraph 26(a)): Practices in this context may include, for instance, efforts to reduce the undertaking’s water and electricity consumption, to reduce GHG emissions or to prevent pollution, and initiatives to improve product safety as well as current initiatives to improve working conditions and equal treatment in the workplace, sustainability training for the undertaking’s workforce and partnerships related to sustainability projects.

Policies (Appendix A: Defined terms): A set or framework of general objectives and management principles that the undertaking uses for decision-making. A policy implements the undertaking’s strategy or management decisions related to a sustainability issue. Each policy is under the responsibility of defined person(s), specifies its perimeter of application, and includes one or more objectives (linked when applicable to measurable targets). A policy is implemented through actions or action plans. For example, undertakings with less resources may have few (or no) policies formalised in written documents, but this does not necessarily mean they do not have policies. If the undertaking has not yet formalised a policy but has implemented actions or defined targets through which the undertaking seeks to address sustainability issues, it shall disclose them.

Policies (clarifications based on definition above and par. 48, 49 VSME and related guidance): The definition of policy clarifies that formalised policies in SMEs are written. Policies can also be "unwritten" i.e. informal. In this case they coincide with a set of practices or a set of implemented actions or defined targets. |

Future initiatives (paragraph 26(c)): future initiatives or forward-looking plans that are being implemented on sustainability issues.

Targets (Appendix A - Defined terms): Measurable, outcome-oriented and time-bound goals that the SME aims to achieve in relation to sustainability issues. They may be set voluntarily by the SME or derive from legal requirements on the undertaking.

Many undertakings already have practices, policies and future initiatives in place, either due to legal requirements (national and/ or European legal requirements such as the European Energy Performance for Buildings Directive, the EU Whistleblowing Directive, health and safety-related national laws, etc.), management of business risks, or as part of their value proposition.

When reporting on their practices, policies, and future initiatives, undertakings may adapt the presentation to their operational organisation, without strict separation between Environment, Social, and Governance topics.

Section 1: Examples of practices, policies, and future initiatives

The examples in dropdown below are sector-agnostic and do not take into account the specificities of sectors, geographical dimensions, or business models. SMEs are encouraged to adapt the examples in Section 1 to their specificities, sector and geography.

This list serves to provide practical illustrations of what Small and Medium Undertakings (11-250 employees) could report under disclosure C2 for practices (current or past), policies (current or past) and future initiatives if they have them in place.

It should be noted that the same examples can also be used by micro undertakings, even though undertakings below 10 employees are in principle not expected to use the Comprehensive Module. They may look at the initial part of the list (less complex), while examples at the end of the list are better suited for medium undertakings.

The list of examples of practices, policies, and future initiatives provided in this supporting guide (Section 1) have been arranged in order gradual increasing complexity.

Subcategory Tables

Pick a topic from the dropdown. Each table displays subcategory columns and the example items you provided (or similar examples) organized by lettered rows.

Examples of practices, policies, and future initiatives

Section 2: Case Studies

This section contains 5 case studies that are based on the list of examples of practices, polices, and future initiatives (from section 1).

The case studies cover different business sectors, each giving an example for small (12 employees) and medium (200 employees) undertaking. The case studies are given in the form of mock-up disclosure. The aim of these case studies is to show how undertakings could disclose C2-related information.

The sectors of the case studies below have been chosen according to the distribution of the main SME sectors in the EU (Eurostat’s Structural Business Statistics (2022)).

Case Study | Reference Sector | Sector share (%) of total SMEs |

| Case Study 1 - Food & beverage: Ready-made meals shop or chain | Wholesale & Retail Trade | 18% |

| Case Study 2 - Manufacturing: Automotive parts producer | Manufacturing | 7% |

| Case study 3 - Agriculture: Milk and dairy producer | Others | <9% |

| Case Study 4 - Construction: Housing construction company | Constructions | 12% |

| Case Study 5 - E-commerce / Digital services: Online retailer | Wholesale & Retail Trade | 18% |

Table 1: Eurostat’s Structural Business Statistics (2022)

Case Study 1

Case Study 2

Case study 3

Case Study 4