EFRAG Today

Areas of interest in this section:

General presentation

EFRAG is a private association established in 2001 with the encouragement of the European Commission to serve the public interest. EFRAG extended its mission in 2022 following the new role assigned to EFRAG in the CSRD, providing Technical Advice to the European Commission in the form of fully prepared draft EU Sustainability Reporting Standards and/or draft amendments to these Standards. Its Member Organisations are European stakeholders and National Organisations and Civil Society Organisations. EFRAG’s activities are organised in two pillars: A Financial Reporting Pillar: influencing the development of IFRS Standards from a European perspective and how they contribute to the efficiency of capital markets and providing endorsement advice on (amendments to) IFRS Standards to the European Commission. Secondly, a Sustainability Reporting Pillar: developing draft EU Sustainability Reporting Standards, and related amendments for the European Commission.

back to top

Mission statement

EFRAG’s mission is to serve the European public interest in both financial and sustainability reporting by developing and promoting European views in the field of corporate reporting. EFRAG builds on and contributes to the progress in corporate reporting.

In its financial reporting activities, EFRAG ensures that the European views are properly considered in the IASB’s standard-setting process and in related international debates. EFRAG ultimately provides advice to the European Commission on whether newly issued or amended IFRS Standards meet the criteria of the IAS Regulation for endorsement for use in the EU, including whether endorsement would be conducive to the European public good.

In its sustainability reporting activities, EFRAG provides technical advice to the European Commission in the form of draft European Sustainability Reporting Standards (ESRS) elaborated under a robust due process and supports the effective implementation of ESRS.

EFRAG seeks input from all stakeholders and obtains evidence about specific European circumstances throughout the standard-setting process. Its legitimacy is built on excellence, transparency, governance, due process, public accountability and thought leadership. This enables EFRAG to speak convincingly, clearly, and consistently, and be recognised as the European voice in corporate reporting and a contributor to global progress in corporate reporting.

back to top

EFRAG Structure

back to top

Public accountability

Public accountability is ensured on the one hand by EFRAG's governance and on the other by EFRAG's due process. EFRAG is accountable to the public at large and the European institutions through its open and transparent due process ( including public consultation on its positions); the transparency of EFRAG's work; and the public meetings of :

• the Financial Reporting and Sustainability Reporting Boards;

• the EFRAG Financial Reporting and Sustainability Reporting Technical Expert Groups;

• their public agenda papers and open nomination processes.

EFRAG publishes an Annual Review yearly discussing its activities and presenting the audited financials of the past year. The funding by the European Commission brings enhanced scrutiny of EFRAG's activities and expenses, including detailed activity reports to the European Commission.

back to top

Funding of EFRAG

EFRAG's funding originates from both the public sector (the European Union) and the private sector (EFRAG's Member Organisations). Funding by the European Commission is granted through yearly grant agreements. Funding by the Member Organisations includes both contributions in cash (provided to EFRAG in accordance with EFRAG's bylaws), in-kind secondments to the EFRAG technical staff and other forms of in-kind contributions (membership of various groups –EFRAG Administrative Board, EFRAG Financial Reporting and Sustainability Reporting Boards, EFRAG Financial Reporting and Sustainability Reporting TEGs, and their working groups, advisory panels, and project task forces – free of charge). The EFRAG Administrative Board President and EFRAG Financial Reporting and Sustainability Reporting Chairs may be remunerated. The EFRAG Financial Reporting and Sustainability Reporting TEG Chairs and CEO are employees of EFRAG.

EFRAG is co-funded by the European Union and EEA and EFTA countries. The contents of EFRAG’s work and the views and positions expressed are however the sole responsibility of EFRAG and do not necessarily reflect those of the European Union or the Directorate-General for Financial Stability, Financial Services and Capital Markets Union (DG FISMA). Neither the European Union nor DG FISMA can be held responsible for them.

back to top

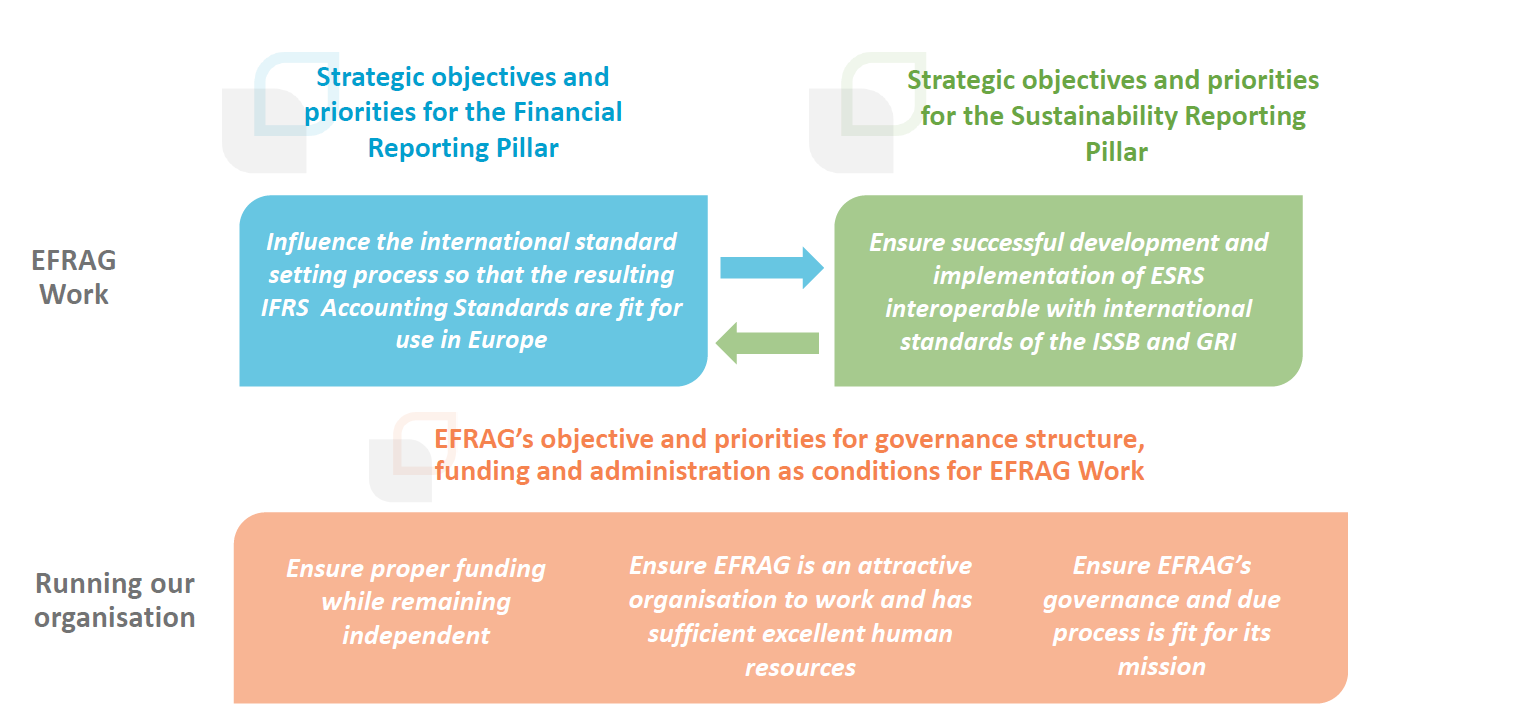

EFRAG Strategy 2024-2027

The EFRAG organisation is growing as a result of its expanded mission, including a new pillar on sustainability reporting, an expanded governance structure, an extended membership, an increased staff base, and new topics in the work plan such as connectivity. These changes represent a significant expansion of EFRAG's activities and they pose new challenges and opportunities for EFRAG and set new conditions for the success of EFRAG.

As Europe's voice in corporate reporting, EFRAG's overall objective is to further develop its thought leadership and key contributions to the development of high-quality corporate reporting in Europe and worldwide. This objective is fundamental to allow the consensus views of relevant European stakeholders to be heard in the process. This leads to the European public interest being considered in the international corporate reporting debate and standard setting process and supports the achievement of European policy goals.

EFRAG's 2024-2027 Strategy outlines specific goals and objectives to be achieved in the next four years and serves as a roadmap for EFRAG to navigate through the challenging and rapidly changing environment. This Strategy will, among other things, guide and help EFRAG in identifying priorities, deciding on how to use its resources efficiently, and making informed decisions. It will also help all those working with EFRAG (i.e., EFRAG Member Organisations, working groups, staff, etc) understand what EFRAG wants to achieve and, consequently, align efforts towards common targets and goals.

The EFRAG 2024-2027 Strategy is divided into two main areas:

Strategic objectives and priorities related to EFRAG's technical work and advice to the European Commission, which encompasses a financial reporting and sustainability reporting pillar.

Objectives and priorities related to EFRAG's governance structure, funding and administration as conditions for EFRAG's technical work and advice to the European. These will help in ensuring that future IFRS Accounting Standards are endorsed and European Sustainability Reporting Standards (ESRS) are developed using an inclusive and rigorous due process and that EFRAG is an attractive organisation to work for now and in the future. These goals and objectives are particularly important so that EFRAG can effectively manage the aftermath of its governance reform, which integrated the sustainability reporting pillar into the EFRAG governance structure.

The EFRAG Strategy 2024-2027 is available here.

back to top

Building strong influence beyond the borders of Europe

Financial Reporting Activities

EFRAG is a member of the European delegation to the IASB Accounting Standards Advisory Forum (ASAF), a member of the International Forum of Accounting Standard Setters (IFASS) and has bilateral relationships with regional or national groups interested and involved in IFRS development. EFRAG also participates in the World Standard Setters meeting. EFRAG provides the Chairmanship and technical secretariat support for the period 2022 – 2024 of IFASS. IFASS is chaired by the EFRAG Financial Reporting TEG Chairwoman. The EFRAG CEO is a member of the IFRS Advisory Council. Whilst EFRAG's draft comment letters are published as a basis for EFRAG's due process in Europe, it is widely acknowledged that they attract interest way beyond Europe.

Furthermore, EFRAG enjoys a constructive relationship with the IASB in many ways: EFRAG welcomes IASB members and staff as observers to the EFRAG Financial Reporting TEG and its Working Group meetings; EFRAG staff cooperates with the IASB staff on a frequent basis; the IASB participates in outreach events and field-testing organised by EFRAG in partnership with National Standard Setters in Europe and European stakeholder Organisations; and EFRAG and IASB leadership meet privately on a regular basis.

Sustainability Reporting Activities

EFRAG is in process of implementing the sustainability reporting governance structure including the technical bodies aiming to be operational by the end of March 2022. The sustainability reporting standard-setting work is carried out on a project basis by the Project Task Force on European Sustainability Reporting Standards (PTF-ESRS). The PTF-ESRS entered into cooperation agreements with GRI, Shift and WICI and had meetings with the IFRS Foundation’s Technical Readiness Working Group. The cooperation with relevant international and European initiatives in the sustainability reporting (standard-setting domain), including the ISSB is envisaged to be continued in the EFRAG permanent governance structure.